Portugal

VAT Basics

Portugal has opted for the reduced VAT rates on a number of items allowed by the VAT Directive.

VAT rates by goods and services in Portugal

The standard VAT rate is 23%. The standard VAT rate generally applies for all goods and services for which no exemption, 0% or one of the reduced VAT rates is foreseen.

The first reduced VAT rate is 13%. This reduced rate applies to certain food products and wine, certain types of fossil fuels, as well as musical instruments, among others.

In addition, there is a reduced VAT rate of 6%. This reduced rate applies to basic food products, certain books, and newspapers, some pharmaceutical products, medical equipment, passenger transport, and hotel accommodation, among others.

Supplies and services at 0% are the standard supplies, such as exports or intra-Community supplies.

Finally, some supplies are VAT exempt, such as health services, public education, and financial services, among others.

To confirm the VAT rate applicable to your product or service in Portugal, we recommend that you contact us.

VAT deduction limits in Portugal

Input VAT is generally deductible as long as the goods or services are used for business purposes.

According to the national legislation, in particular article 21 of the Portuguese VAT Code, following expenses are excluded from the right to deduct:

- Acquisition/hiring/use/transformation/repair/manufacturing or import of passenger cars, pleasure crafts, helicopters, planes, motorcycles, except for goods which sale or exploitation is the object of activity;

- Fuel:

- Petrol

- Partially deductible (50%) - diesel, LPG, natural gas and biofuels, except

- Fully deductible (100%) - diesel, petrol, LPG, natural gas and biofuels, in the case of: Heavy passenger vehicles; Vehicles licensed for public transport, rent-a-car vehicles excluded; Diesel; LPG, natural gas or biofuel consuming machines, which are not registered vehicles; Tractors exclusively or predominantly used for fieldwork related to agricultural activity; Vehicles transporting goods, weighting more than 3 500Kg.

- Business travels made by taxable person and staff, including toll fees.

- Food, accommodation, beverages and tobacco, except in cases the expense is related to conferences, fairs, expositions or congresses, where a deduction of 50% or 25% can be applied, according to the Portuguese VAT Code (Art. 21, paragraph 2, Portuguese VAT Code).

- Fun and luxury, not considered normal operating expenses.

A valid and fully compliant VAT invoice must be issued for each expense on which VAT is deducted.

The VAT deduction limits in Portugal are regulated in Article 21 CIVA.

Statute of Limitations in Portugal

The statute of limitations in Portugal is four years, counted from the beginning of the natural year following the date when the VAT became deductible or due.

The statute of limitations period determines the periods on which the tax authority can go back to review the information declared, and apply additional VAT assessments, penalties or interests. Also, the statute of limitations determines the period a taxpayer can voluntarily correct any errors on past submissions, and deduct input VAT. There is a limit to arithmetical errors, which is two years for making these corrections.

Tax point rules in Portugal

The tax point is the time when VAT becomes due. VAT due should be distinguished from VAT payable. VAT is due when the tax point occurs. VAT is payable between the day after the end of the reporting period and the due date to submit and pay the VAT return.

- General rule: When the supply of goods or services is subject to the mandatory issuance of an invoice, then the tax point is by the time the invoice is issued, or should have been issued. Otherwise, VAT becomes due when the goods are put at the customer’s disposal, or when the services are completed.

- Prepayments or advanced payments create a tax point because an invoice must be issued for each instalment or prepayment.

- Intra-Community acquisitions: Tax point occurs on the invoice date or the 15th day of the month following the month in which the invoice was issued, whichever occurs earlier. This rule does not apply in case of partial advanced payments prior to the moment in which the goods are placed at the customer’s disposal.

- Import: Tax point occurs when the goods are imported according to the relevant import documents.

Tax point rules in Portugal are regulated in Articles 7 and 8 CIVA.

Use and enjoyment rules in Portugal

When it comes to establishing the place of supply of a transaction, Member states may introduce another exception to the B2B rule according to the place where the services have been used and enjoyed. This exception may be introduced to avoid double taxation (positive use and enjoyment rules), to avoid non-taxation (negative use and enjoyment rules), or both.

Portugal introduced the negative use and enjoyment rule, hence attracting the place of supply to Portugal. This concerns the supplies of services when provided by a Supplier established in a country outside the EU to final customers (B2C) established in Portugal, provided that the services are used and enjoyed in this country in the following scenarios.

- Lease of tangible movable assets B2C made to a person established or domiciled outside the EU, when the actual use or exploitation of these assets occurs in national territory.

- Short-term lease of a means of transport B2C when the transport is put at the customer’s disposal outside the Community and the effective use or exploitation of the means of transport occurs in the national territory.

- Lease of means of transport B2C, other than short-term leasing, when it is established or domiciled outside the Community and the effective use or exploitation of the means of transport occurs in the national territory.

Separately, the use and enjoyment rules apply for telecommunications, broadcasting and electronic services (TBE services) in Portugal when these services are supplied to a customer established outside the EU but the actual use and enjoyment takes place in Portugal.

Portuguese Bad Debt Relief

Bad debt regime applies on sales where an invoice has been issued with VAT, reported in the VAT return and the VAT amount has been paid to the tax authorities but the whole price has not been collected from the customer.

This is often due to the client´s bankruptcy, insolvency or simple missed payments to suppliers. In these cases, most countries allow to recover the VAT initially paid to the authorities, however, the conditions change from one country to another.

Portugal allows for bad debt relief by adjusting the out VAT paid in the periodic VAT return. In order to be able to deduct the bad debt, also known as créditos de cobrança duvidosa in the local language:

- The credit is overdue for more than 12 months and there are proofs about the payment being due.

- The credit is overdue for more than 6 months when the debtor is a private individual or a VAT exempt taxable person without the right to deduct VAT, provided that the VAT credit per invoice is not higher than EUR 750.

- Also, the bad debt relief is allowed before those timelines in case of execution procedures or insolvency.

The bad debt relief regime is regulated in Article 78 CIVA.

VAT Registrations and Simplifications in Portugal

When do I need a Portuguese VAT number?

Generally, a foreign business must register for VAT in Portugal as soon as a taxable supply is made. The following are the usual examples of taxable transactions:

- Domestic supply of goods not reverse charged: A supply of goods located in the Portugal where reverse charge does not apply requires a VAT registration of the supplier.

- Supply of services not reverse charged: Foreign non-established businesses supplying services on which Portuguese VAT is due by the supplier must register for VAT. These services are rather exceptional, as the general B2B rule would apply.

- Export: Exporting goods to a non-EU country requires a VAT number before the export is made.

- Intra-Community acquisition: Acquiring goods from another Member State where all conditions for intra-Community movements are met requires the customer to register for VAT.

- Intra-Community supply: Supplying goods another Member State is also a taxable transaction that obliges the supplier to register for VAT.

- Distance sales: When applicable in case the Seller has not joined OSS. See the E-commerce manual for more information.

Backdated registrations are possible in Portugal. However, this involves the payment of a penalty at the moment of registration.

There is no registration threshold for Portuguese established companies. All companies must submit a declaration of commencement of activities (Declaração de início de atividade) before performing any taxable transactions, as indicated in articles 29 and 31.1 CIVA. The only exception to this rule is that the entities performing sporadic transactions which do not exceed EUR 25,000 (atos isolados). When these entities exceed the EUR 25,000 threshold, the need to VAT register, although they are exempted from submitting periodic VAT returns.

Input VAT incurred previous to the VAT registration may be deducted in certain circumstances, provided that the cost complies with the VAT deduction limits in Portugal. This input VAT will be included in the first VAT return submitted by the taxpayer.

Fiscal representative requirements in Portugal

Non-EU businesses need to appoint a fiscal representative when registering for VAT purposes in Portugal. For businesses established in the EU and the European Economic Area (EEA) the appointment of a Portuguese fiscal representative is just optional.

Marosa provides the fiscal representation service through our Portuguese entity.

The requirement for non-EU businesses of appointing a fiscal representative is regulated in the local legislation in art. 126.º do CIRC e art. 19.º da LGT.

VAT Groups in Portugal

VAT grouping is not possible at the moment in Portugal.

Consignment and Call-off stock in Portugal

The EU introduced a call-off stock simplification that all EU Member States must implement. This was put into place so that businesses that operate under a consignment stock structure do not have to VAT register in the country of destination. Portugal has introduced the consignment stock simplification.

Check out our article on the EU call-off stock simplified VAT rules for more detailed information.

Portuguese Import Deferral and Postponed VAT Accounting.

Portugal has introduced a postponed import VAT accounting mechanism where import VAT can be reported as input and output VAT (reverse charged) in the VAT return instead of being paid to the authorities upon importation.

Import VAT deferral, meaning delaying the payment of VAT for a given period, is not applicable in Portugal. You should however be aware of the difference as postponed import VAT accounting is sometimes referred as deferral import VAT.

For postponed import VAT accounting to apply, a business must meet the following criterium:

- Submit VAT returns on a monthly basis;

- Should not have any outstanding tax debts;

- Only carry out transactions which are subject to VAT, or exempt transactions with the full right to deduct the input VAT.

The application shall be submitted by the 15th day of the month previous to the desired start of the postponed import VAT accounting application.

Have a look at our general article about postponed import VAT accounting.

Portuguese Customs and VAT warehouses

Customs or bonded warehouses are available for goods that have not cleared customs in the EU (T1). VAT and excise duties are not due when these goods are directly placed in the Customs warehouse. As soon as they exit this regime, these amounts are due. Sales within the customs warehouse are zero-rated.

VAT warehouses are available for cleared goods (T2). These goods have already paid customs duties. The conditions are similar to those of Customs warehouses. The goods allowed are those included in Appendix V of the VAT Directive. In addition, the following goods may also be subject to this suspension regime: certain wood items, gold, iron and steel product and non-ferrous metal.

Find here more information about special customs regimes in Portugal.

Finally, find here official EU guidelines on Customs’ special regimes.

Special VAT Schemes in Portugal

There are two different VAT schemes for small businesses in Portugal:

- The exemption scheme, or Regime de isenção, (Article 53 CIVA) and

- Simplified scheme for small retailers, or Regime dos pequenos retalhistas (Article 60 CIVA).

Apart from the above special VAT schemes for small businesses, there are the following special VAT schemes in Portugal:

- Farmers

- Travel agents

- Margin scheme

- Investment gold

The special VAT schemes applicable in Portugal are regulated in Section IV CIVA.

Reverse Charge in Portugal

Reverse charge for non-established companies in Portugal

According to art 194 of the VAT Directive, Member States may implement an optional reverse charge on supplies made by non-established businesses. Portugal has introduced this reverse charge on supplies of goods and services located in Portugal.

Where a non-established supplier, without a fiscal representative appointed, supplies goods or provides services located in Portugal to a VAT registered and established customer, the domestic reverse charge applies. It is not relevant if the supplier is registered or not.

The domestic reverse charge on services is rather exceptional as it would only apply where the B2B rule on services does not apply. This is, for example, the case for supplies of services connected to immoveable property.

Additionally, there is a specific reverse charge on supplies of natural gas, electricity, heat and cooling energy supplied by non-established suppliers to taxable dealers established in Portugal.

The reverse charge on supplies made by non-established companies is regulated in Article 2.1º.g) CIVA. Also, the reverse charge on supplies of gas, electricity, heat and cooling energy supplied by non-resident suppliers to taxable dealers is regulated in Article 2.1º.h) CIVA. Also, find here the FAQ published by the PT TAs about reverse charge.

Reverse charge in B2B services

Article 196 of the VAT Directive requires the reverse charge mechanism on all services subject to the B2B rule introduced in art. 44 of the same Directive. The B2B rule locates the transaction where the business customer is located. In case the customer is a private individual, B2C rules locate the transaction where the supplier is located.

According to the general B2B rule, any business resident outside Portugal supplying services to a Portuguese based customer will not charge any VAT and the transaction will be reverse charged by the customer.

There are however a number of exceptions to this rule. Where these exceptions apply, reverse charge is still applicable in Portugal provided the following conditions are met:

- Services connected to immoveable property are located where the property is located.

- Passenger transport services will be located where the transport takes places (apportioned if necessary).

- Catering services are located where the catering takes place.

- Short term leasing of means of transport are located where the vehicle put at the disposal of the customer.

- Access to conferences, fairs and exhibitions is located where the event takes place.

The general rule may also be deviated where the supplier has a permanent establishment in the country of the customer and the PE has intervened in the supply.

Find out more about the rules for B2B services in the EU here.

Reverse charge on specific goods and services in Portugal

Domestic reverse charge may also apply on the supplies of certain goods and services located in Portugal.

- Construction work including repair, cleaning, maintenance, alteration and demolition services in relation to immovable property, including the handing over of construction works. Article 2.1º.j) CIVA. This reverse charge applies only when the customer is established, or has a permanent establishment, in Portugal.

- Immovable property (where opted to tax).

- Transfer of CO2 emission allowances. Article 2.1º.l) CIVA.

- Used materials, scrap and waste, Article 2.1º.i) CIVA.

- Supplies of forestry goods including cork, wood, pine cones and pine nuts with bark. Article 2.1º.m) CIVA. This reverse charge applies only when the customer is established, or has a permanent establishment, in Portugal.

- Supplies of electricity produced in units for self-production. Article 2.1º.n) CIVA. This reverse charge applies only when the customer is established, or has a permanent establishment, in Portugal.

VAT Returns in Portugal

Frequency of VAT returns in Portugal

The frequency of filing of the periodic VAT returns depends on the annual turnover of the previous year in Portugal.

Monthly VAT returns are due when the taxpayer reached or exceed the turnover threshold of EUR 650,000 in the previous calendar year. If the annual turnover in the previous calendar year is below EUR 650,000, then the VAT returns are due on a quarterly basis. Similarly, for new VAT registrations, the filing frequency will be assigned based on the estimated annual turnover declared in the registration form.

Additionally, businesses VAT registered in Portugal must submit an annual VAT return, a recapitulative statement.

The following reporting periods apply under the normal regime:

Due date of Portuguese VAT returns

Deadlines are different for VAT return submissions and VAT payments linked to these returns.

More information about due dates for making VAT payments and submitting the periodic VAT returns is available in the tax calendar published at the website of the tax authorities.

Deadlines and frequency of filing are regulated in Article 41 CIVA.

VAT payments in Portugal

Non-established companies will often make payments from an overseas bank account. The following details are used for paying taxes from abroad when you choose the method of paying via bank transfer:

- Name of the recipient: Autoridade Tributária e Aduaneira

- IBAN code: PT50 0781 0019 00000008369 27

- SWIFT code: IGCPPTPL

- Name of the bank: Agência de Gestão da Tesouraria e da Dívida Pública – IGCP, E.P.E

- Reference: Each reference corresponds to a specific number for payment, which is set out in the document generated after the submission of the VAT return. Also, it is mandatory to quote the taxpayer's Portuguese VAT number (NIF). You may follow this structure: NIF 98XXXXXXX/ unique reference

Have a look here at the information leaflet of the PTA about how to pay taxes from abroad in Portugal. Also, here you will find more information about VAT payments.

VAT refunds in Portugal

In principle, the excess of input VAT is carried forward to the next reporting period. This is, when a taxable person declares more VAT deductible – eg., due to purchases-, than VAT collected from sales, the difference is a VAT credit which shall be carried forward to the following period to compensate with future output VAT.

However, you can apply for a VAT refund of the VAT credit reported in your VAT return in the following scenarios:

- The VAT refund amount exceeds EUR 3,000;

- After 12 months, the VAT credit exceeds EUR 250;

- In case the business will cease activities and the value of the refund is higher than EUR 25.

When the amount of VAT credit exceeds EUR 30,000, the tax authorities may require the taxpayer to setup a bank guarantee for a period of six months.

This is regulated in article 22 CIVA.

Nil and corrective VAT returns in Portugal

A nil VAT return needs to be submitted even if there are no transactions to be reported for that period.

Errors or omissions in a VAT return (periodic or annual) must be corrected. You will need to submit a substitutive VAT return, i.e., a VAT return including all the amounts corresponding to the transactions performed during the period, not only those related to the amendment. When preparing the corrective VAT return, you will need to indicate that the return is “out of date”, as well as the reporting period to which the correction refers to.

Also, when the mistake that you are correcting is due to the overpayment of VAT, the correction is optional and must be made within a period of two years.

Have a look at Article 78 CIVA.

Additionally, you will find more information about corrective VAT returns under the following link. The corresponding question about VAT corrections includes the following feedback: “Deverá submeter uma nova declaração do IVA para o período pretendido, através do endereço www.portaldasfinancas.gov.pt, preenchendo todos os campos em que tenha havido movimento no período (e não só os que pretende corrigir)”.

Annual VAT Returns in Portugal

Most companies must submit an annual VAT return in Portugal by the 15th of July of the following year. Please consider that in case of VAT de-registration in Portugal, the last annual VAT return is subject to a shorter deadline: by the last day of the third month after the de-registration date. This is a recapitulative statement which contains all the information reported during the year.

The annual VAT return must be submitted via the tax authorities’ website, the same as for the periodic VAT returns.

VAT penalties in Portugal

The above penalties are regulated in Article 114 and 116 RGIT (REGIME GERAL DAS INFRAÇÕES TRIBUTÁRIAS).

Portuguese Tax Authorities Contact

Autoridade Tributária e Aduaneira (AT)

- Phone: 217 206 707, at working days from 9h to 19h

- Online contact form.

Useful links:

- E-balcao access.

- General fiscal information. Also, find here the Despachos and here the Ofícios circulados IVA or administrative orders issued by the Portuguese tax authority.

- Portuguese VAT Law (Código do Imposto sobre o Valor Acrescentado or CIVA).

- Taxpayer’s Support.

- Find the current VAT forms.

Intrastat Contact

Email contact: intrastat@ine.pt ; fernanda.sengo@ine.pt

Customs Contact

Direção de Serviços de Regulação Aduaneira (DSRA)

Rua da Alfândega, n.º 5 r/c

1149-006 Lisboa

Telefone 217 206 707 (Opção 2 – 1 – 1)

Horário: das 09h00 às 13h00 e das 14h00 às 17h00

Email: dsra@at.gov.pt

Helpdesk EORI: dsra-eori@at.gov.pt

ESL Returns in Portugal

Due date and frequency of ESL returns in Portugal

The due date for submitting monthly or quarterly ESL returns is always the 20th day of the following month.

The frequency of filing depends on the reporting periods for VAT as well as on the turnover of intra-Community transactions.

Find here the taxpayer’s calendar published by the Portuguese tax authorities, where the ESL returns are included.

Nil and corrective ESL returns in Portugal

If there are no intra-Community transactions to be reported in a given period, a nil ESL is NOT due.

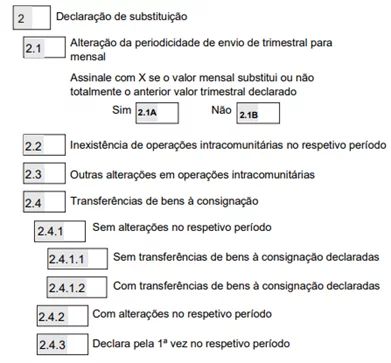

Corrective ESL returns in Portugal are prepared and submitted electronically by ticking the option 2 in the form: Declaração de substituição. Then you will need to choose the reason for submitting the corrective ESL return by ticking one of the following 4 boxes and corresponding sections within each one.

- Field 2.1, when you have changed the frequency of filing from quarterly to monthly (this field must be completed when the threshold of €50,000 is exceeded). This field concerns exclusively intra-community transmissions of goods and similar operations.If you tick this field, you must indicate whether the amount to be declared in that month completely replaces, or not, the amount already declared for the quarter to which that month belongs (2.1A or 2.1B).

- Field 2.2, due to the lack of intra-community operations in the respective period (this field must be completed when, having completed Table 04, it is verified that, in that period, there are no operations to be declared due to: cancellation of the operation, regularization or any other occurrence).

- Field 2.3, for any other changes verified in relation to Tables 04 and 05 of the previously sent declaration (corrections to the amounts declared in relation to intra-community operations, as a result of regularizations, omissions or rectification of invoices, change of the NIF of the acquirer, of the Member State of destination or prefix, etc.).

- Field 2.4: Field exclusively intended to indicate the occurrence during the period of intra-community transfers of consignment goods to be detailed in Table 06. Mandatory field to be completed whenever submitting a summary replacement declaration, and if there are no transfers in the period, the fields 2.4.1 and 2.4.1.1.

Penalties for late ESL returns in Portugal

The same penalties as for VAT and Intrastat returns apply. The late submission of ESL returns is punished with a penalty ranging from EUR 150 to EUR 3,750.

The above penalties are regulated in Article 116 RGIT (REGIME GERAL DAS INFRAÇÕES TRIBUTÁRIAS).

Intrastat Returns in Portugal

Frequency of filing and due date of Intrastat returns in Portugal

Like in most EU countries, Portuguese Intrastat returns are filed monthly. They follow the calendar month. The due date to file these returns is the 15th day of the following month.

Portuguese Intrastat thresholds

The following annual Intrastat thresholds apply in Portugal (calendar year) for 2026:

Type of Intrastat: standard declaration

- Arrivals EUR 600,000

- Dispatches EUR 600,000

Separately, Intra-Union operators based in Autonomous Region of Madeira that have recorded, in the last 12 available months (at the time of the sample selection) Arrivals and/or Dispatches of a value equal or above EUR 25 000, must provide statistical information.

Additionally, there is a second threshold to submit a detailed Intrastat declaration, which is the same for both flows: EUR 6,499,999.

These thresholds are computed annually according to the calendar year. Once filed, a complete calendar year needs to be covered by a company in order to stop filing these returns. For example, if a company exceeds the threshold in March 2024 on arrivals, Intrastat returns for arrivals are due until December 2025. These thresholds are calculated according to the invoice value. The authorities monitor the thresholds and often send letters to each taxpayer requiring them to file missing Intrastat return.

Have a look at our overview of Intrastat thresholds.

Also, find here official information.

Reporting of specific scenarios in Portugal

Very often, the transactions reported in the Intrastat return are standard sales from one taxable person to another. However, a number of scenarios have specific reporting requirements. The nature of transaction code in the Portugal have been recently updated and have now two digits. See the official Intrastat manual under the following link. It contains the nature of transaction for the reporting of specific scenarios.

Nil and corrective Intrastat returns in Portugal

If no transactions are to be reported, a nil Intrastat return must be filed, selecting as declaration type: "Ausência".

Regarding corrections, if an Intrastat return has been submitted showing wrong or incomplete information, a new return needs to be submitted electronically correcting the wrong data and adding the data initially missed. This is done by submitting a declaração de substituição correcting the corresponding transaction.

You should follow this procedure:

- Open the respective declaration already submitted, clicking on "Fill out a replacement declaration" (or Preencher uma declaração de substituição);

- Then the previous lines are automatically recovered and you can make the necessary changes: edit, add or delete the desired lines and click again in "reply" (responder).

Intrastat Penalties in Portugal

The same penalties as for VAT and ESL returns apply. The late submission of Intrastat returns is punished with a penalty ranging from EUR 150 to EUR 3,750.

The above penalties are regulated in Article 116 RGIT (REGIME GERAL DAS INFRAÇÕES TRIBUTÁRIAS).