Poland introduces VAT split payment mechanism

Poland will introduce a voluntary VAT split payment mechanism as from 2018.

This system will only apply on domestic transactions and will not affect invoice requirements. B2C transactions will not be impacted by these changes, only business to business sales. We have not received information about the possibility of opting for this mechanism by non-established entities who are VAT registered in Poland.

What is the VAT split payment mechanism?

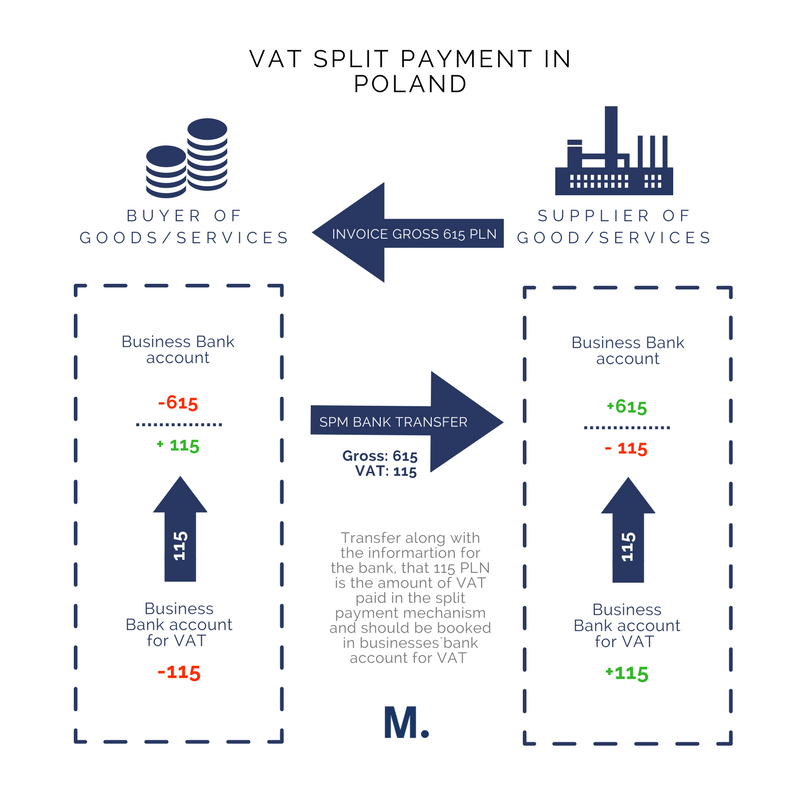

Under the usual rules of VAT, the supplier issues an invoice for the net and VAT amount to the customer; the customer will pay the gross amount (net and VAT) to the supplier, who will collect it and pay it to the tax authorities. Under the split VAT payment mechanism, the supplier also issues an invoice for the net and VAT amounts, however, the customer will only pay the net amount to the supplier. The VAT portion is paid directly to the tax authorities, hence eliminating the ´collection´ role of suppliers.

Because it is a voluntary regime in Poland, the European Commission is not required to approve this system. Italy introduced a similar mechanism on supplies to public entities. In this case, the Commission recently allowed an extension of this regime.

Mechanics of the new system in Poland

In Poland, every business who voluntarily opts for the split payment mechanism will have at least two bank accounts: Their usual bank account where they receive payments for their day a day business; and a VAT bank account where they must pay VAT on their purchases. This system requires strong cooperation from banks and financial institutions.

Incentives for using VAT split payment

Those taxpayers opting for the new split VAT payment mechanism by the end of the year will benefit from a number of simplifications on their tax compliance: Penalties are reduced where most input VAT is ´paid´ with this system; VAT refunds will be received as early as 25 days from the moment the VAT is transferred to the VAT bank account; joint tax liability of the customer is cancelled when supplying certain goods such as IT equipment, fuel and others; and there is an extra repayment for payment VAT earlier than the statutory deadline.

We will call you back

Give us your contact details and our team will contact you to organize a demo and evaluate how you can integrate your system with our tool.