Spain introduces plastic tax

Spain will introduce a plastic tax on non-reusable plastic packaging from January 2023, potentially affecting foreign businesses operating in the country.

## Update June 2023: the Spanish tax authorities published a binding decision confirming that the Spanish plastic tax amount is included in the taxable base of the intra-Community acquisitions transactions. This confirmation is included in the Binding decision n.º V1534-23, dated 5 June 2023.

Spanish plastic tax introduction

Spain introduced the plastic tax on non-reusable plastic packaging, following the global trend of green taxes. It is effective since January 2023.

In accordance with the EU requirements, Spain has implemented the plastic tax – as part of Law 7/2022, dated 8th April with a broader scope, which aims to tax the following “non-reusable” plastics:

- Non-reusable plastic containers.

- Semi-finished plastic products intended for the production of non-reusable plastic packaging.

- Plastic products intended to allow the closure, trading or presentation of the non-reusable containers.

Some products are exempt or zero rated. This is the case, for example, of the plastic packaging for pharmaceutical products, and other types of goods that are related to health care and hospital use; when the plastic packaging is sent outside the Spanish territory; when the product introduced in the country will be destroyed or is inadequate for its use, or in case of low volume intra-community acquisitions and imports – when the non-reusable plastic packaging weight does not exceed 5kg per month. However, there are formal obligations that still remain in case of exempt or zero rated transactions.

Also, a deduction and refund systems are put into place to avoid double taxation and ensure the application of the exemptions described in the Law.

Spanish tax authorities have published a Frequently Asked Questions article about this new tax.

Have a look at our article about the Frequently Asked Questions on Spanish Plastic Tax. It includes a link to our dedicated webinar and other useful materials.

What is the taxable event, tax point and taxable base of the Spanish plastic tax?

The Spanish plastic tax applies on the following transactions involving the above-described non-reusable plastic packaging:

- The manufacture or production of the plastics in scope. The tax point rule in this case occurs when the first delivery is made or made available to the purchaser. In case of advance payments, the tax will be due at the time the total or partial collection of the price is actually received.

- The intra-Community acquisitions of the plastics in scope. The tax is due by the 15th day of the following month the transport was initiated, or by the time the invoice is issued – whatever occurs first.

- The imports of those products. The plastic tax is due when the import is made at customs, in line with the time the custom duties are due. Have a look here at the official information about making imports subject to plastic tax.

- The irregular introduction of those products in Spanish territory.

The taxable base is calculated based on the weight in Kilograms of the non-reusable plastic in scope, and the rate is EUR 0.45 / KG.

The amount of non-reusable plastic subject to taxation will need to be certified by a third party.

In order to apply Spanish plastic tax on imports at Customs, the tax authorities have adapted the imports system. Learn more about these changes in the official notice published by the tax authorities.

Who will be liable for the plastic tax?

In general lines, the sole traders and companies that are producers, intra-Community acquirers, or importers of the goods in scope of the plastic tax.

Foreign taxpayers subject to the Spanish plastic tax must appoint a Spanish representative before performing the first taxable event.

Foreign companies subject to the Spanish plastic tax must appoint a Spanish representative before performing the first taxable event.

The taxpayers producing the product in scope, or making intra-Community acquisitions of it, will have to submit the plastic tax return following the same reporting periods as their periodical VAT returns – either monthly or quarterly. The importers will have to pay the tax at Customs

Taxpayers subject to the Spanish plastic tax must register in the special register for plastic tax, the latest by the 30th January 2023.

Also, the Spanish plastic tax impacts on the invoicing requirements: producers will have to include on the invoice the amount of the tax due, the KG of plastic subject to the tax or, in case an exemption applies, the article of the Law containing such exemption. Also, in the rest of cases, the acquirers shall request their suppliers to include similar data on a certificate or in the invoice received.

Finally, there are accounting obligations related to the Spanish plastic tax:

- In the case of producers, they must keep accounting records for the products manufactured and the materials used for its production.

- Intra-Community acquirers must keep a register of the products.

- The electronic accounting record of the stock must be provided to the Spanish Tax Authorities within one month following the end of the reporting period.

The tax will enter into force by January 2023. We expect the tax authorities publish further guidance on procedures and registration.

How can Marosa help you?

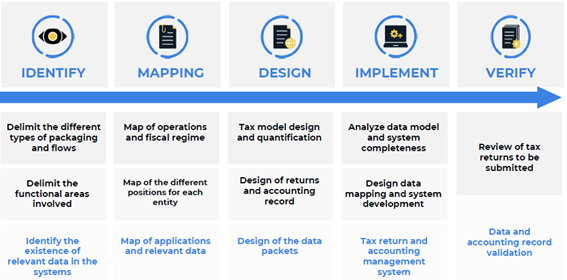

Marosa and Belén Palao Abogados have designed an approach to assess the impact analysis and handling the new reporting obligations on an organization. We will look at the flows, packaging identification, data mapping and generation of files that we will convert to the accounting of stocks. We will also prepare the periodic tax declarations and bookkeeping plastic listings.

Initially, it is required to identify the use of single-use plastic packaging and delimit the purchases and sales flows, including the different functional areas of the organization that may be affected by the tax. Then, the existence of the relevant data in the systems will be verified.

This information will allow us to map the operations and the fiscal regime to design the tax model and its quantification, the different positions for each entity and the systems that store the relevant data.

We will use all these maps to design the tax model and its quantification to define the tax returns and the accounting record of the stock.

The next step involves the analysis of the data model to verify the system completeness. This will allow us to design the data mapping and develop the system to provide the tax return and accounting management system.

Finally, all work will be verified to ensure all steps have been completed successfully.

We will call you back

Give us your contact details and our team will contact you to organize a demo and evaluate how you can integrate your system with our tool.