VAT Rules for dropshipping and E-commerce in EU

This article describes the VAT rules on dropshipping activities in the EU.

This article describes the VAT rules on dropshipping activities in the EU. Although dropshipping is a simple and business-friendly activity, VAT rules make it complex and often require these activities to register for VAT and submit separate VAT returns in each country where your client is located.

What is dropshipping?

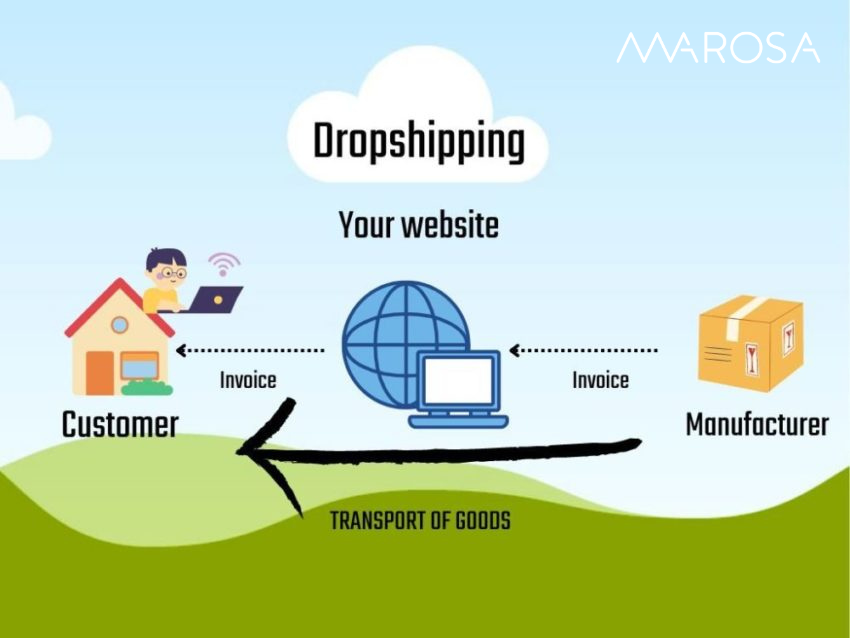

Very often, dropshipping will happen without any storage of your products. So, there is a "flash purchase and sale" when the final customer buys the product. As an example, in these scenarios the flow of events would be as follows: 1) Company A advertises a product online; 2) The final client makes a purchase of this product; 3) Company A buys the product from Company B and requests this company to ship it to the address of the final client; 4) Company A gets an invoice from Company B and issues an invoice to the final client. There are two transactions but only one transport of goods.

In this scenario, you should consider where the goods are coming from and, in case of goods are originally coming from non-EU countries like China or the US, who is in charge of clearing customs on these products. In case the goods come from another EU country, you will normally require a VAT number in either a) the EU country of origin or b) the EU country of destination.

VAT rules for sales within the EU

From a VAT perspective, dropshipping is a chain transaction where the final customer is a private individual. This is a B2B2C scenario.

When the transport of goods occurs within the territory of the same country, the VAT treatment is straightforward. Considering that there is no storage of goods by the intermediary, and following the example from our previous section, we would see the following transactions from a VAT perspective:

- Domestic supply B2B from Company B to Company A. This supply normally will charge VAT. Depending on whether Company B and Company A are local companies or non-established, a reverse charge may apply.

- Domestic supply B2C from Company A to the final customer. This supply will always charge VAT.

If the Intermediary, Company A, is a non-established company in the country where the goods are dispatched, a VAT registration is required so the Intermediary can charge VAT on the sale to the final customer.

VAT rules for cross-border sales within EU

For cross-border sales within the EU, the level of complexity to assess the VAT treatment in a B2B2C scenario is higher. In this case, the goods are transported from an EU country to another where the final customer is located.

Where the three parties are in three different EU Member States (supply chain B2B2C), we must carefully check the VAT rules applicable and also what is the position of the specific EU countries involved, as tax authorities apply different approaches.

In the past, before July 2021 rules for e-commerce, this activity would imply for the Intermediary supplier to perform the following taxable transactions: 1) an intra-Community acquisition in the country of the customer and 2) a domestic sale B2C in the country of the customer. As a consequence, VAT registration was always required in the countries where the final customers were located.

As of July 2021, with the new VAT rules for e-commerce and the introduction of the OSS regimes, the previous VAT treatment may change. In certain cases, it will be allowed the use of the OSS regimes to simplify VAT compliance and mainly avoid multiple VAT registrations in the EU.

We can find reliable guidance on the VAT treatment from the Working paper nr. 1040 of the European Commission. Based on the Commission’s approach, we can differentiate two scenarios:

Scenario 1: where Company A acts as an Intermediary and is not VAT registered in the country of dispatch of the goods, old rules for VAT apply. To act as an Intermediary, according to Article 36a VAT Directive, Company A is in charge of the transport of the goods or someone on their behalf is doing it. In such case, Company A needs to VAT register in each of the countries of its final customers to report:

- an intra-Community acquisition in the country of the customer and,

- a domestic sale B2C in the country of the customer.

Scenario 2: where Company A, acting as an Intermediary, 1) already has a VAT number in the country from where the goods are dispatched by Company B, and 2) Company A provides this VAT number to Company B, we can understand there is:

- a domestic sale from Company B to Company A in the country of dispatch

- an intra-Community distance sale from Company A to the final country in another Member State.

In this scenario, Company A may avoid multiple VAT registrations by joining the Union OSS regime.

Similarly, as a third scenario, if Company A holds stock in the country from where the goods are dispatched to the final customers, then we are before the same VAT treatment than for scenario 2 and OSS regime can be applied.

Do you have to pay VAT on dropshipping?

As a dropshipper, the Company selling to the final customer (B2C) always has to charge VAT on that supply. This is why, either a VAT registration in the country of the final customer or an OSS registration will normally be required.

The VAT collected from the final customer must be paid to the tax authorities upon the submission of the country’s VAT return or the OSS return, which is paid to the authorities in the country of identification for OSS scheme.

How to charge VAT in multiple countries?

You can charge VAT in multiple countries where you are not established by registering for VAT purposes in those EU countries. As a dropshipper, according to our previous explanations, you will have to charge VAT to your final customers. Normally, the VAT rate to be applied is the one from the country of your end customer.

- In order to be able to charge VAT to your customers you need to get a VAT identification number in those countries. Alternatively, in certain scenarios, you may register in OSS. OSS registration must be made in the EU country where you are established or, if you a non-EU business, you can opt to register in one of the countries from where the goods are dispatched.

- Then you need to verify what VAT rate applies to your products in the country of supply. You can check here our overview of VAT rates in the EU.

- Finally, you need to update your invoicing systems to ensure the correct VAT rate is charged in the invoices.

Have a look at our article about VAT registrations in the EU. Also, learn more about the OSS scheme in our e-commerce manual.

Do I need a VAT number for dropshipping in Europe?

Definitely, yes. If you are a non-EU dropshipper you will either need to get a VAT number:

- In each of the countries where your final customers are located, or

- in the countries where goods are dispatched, as well as a Union-OSS registration;

- when the goods are transported from outside the EU, you may have to register for IOSS scheme, or VAT register in each of the countries where goods are imported.

VAT threshold and tax filing for EU Business and non-EU businesses

There is no VAT threshold applicable when you need to comply with VAT compliance obligations abroad. Normally, registration thresholds may apply only to established companies, who can benefit from special regimes or the exemption to comply with VAT obligations. However, non-established companies making taxable transactions abroad – such as sales to final customers, need to register from the first transaction performed.

Also, in case you perform intra-Community distance sales, the EUR 10,000 threshold only applies if certain conditions are met.

Find here an overview of reporting due dates in Europe.

We will call you back

Give us your contact details and our team will contact you to organize a demo and evaluate how you can integrate your system with our tool.