ESL Returns in Portugal

Due date and frequency of ESL returns in Portugal

The due date for submitting monthly or quarterly ESL returns is always the 20th day of the following month.

The frequency of filing depends on the reporting periods for VAT as well as on the turnover of intra-Community transactions.

Find here the taxpayer’s calendar published by the Portuguese tax authorities, where the ESL returns are included.

Nil and corrective ESL returns in Portugal

If there are no intra-Community transactions to be reported in a given period, a nil ESL is NOT due.

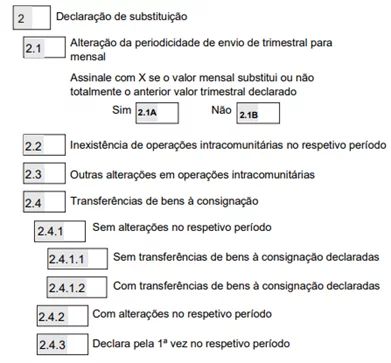

Corrective ESL returns in Portugal are prepared and submitted electronically by ticking the option 2 in the form: Declaração de substituição. Then you will need to choose the reason for submitting the corrective ESL return by ticking one of the following 4 boxes and corresponding sections within each one.

- Field 2.1, when you have changed the frequency of filing from quarterly to monthly (this field must be completed when the threshold of €50,000 is exceeded). This field concerns exclusively intra-community transmissions of goods and similar operations.If you tick this field, you must indicate whether the amount to be declared in that month completely replaces, or not, the amount already declared for the quarter to which that month belongs (2.1A or 2.1B).

- Field 2.2, due to the lack of intra-community operations in the respective period (this field must be completed when, having completed Table 04, it is verified that, in that period, there are no operations to be declared due to: cancellation of the operation, regularization or any other occurrence).

- Field 2.3, for any other changes verified in relation to Tables 04 and 05 of the previously sent declaration (corrections to the amounts declared in relation to intra-community operations, as a result of regularizations, omissions or rectification of invoices, change of the NIF of the acquirer, of the Member State of destination or prefix, etc.).

- Field 2.4: Field exclusively intended to indicate the occurrence during the period of intra-community transfers of consignment goods to be detailed in Table 06. Mandatory field to be completed whenever submitting a summary replacement declaration, and if there are no transfers in the period, the fields 2.4.1 and 2.4.1.1.

Penalties for late ESL returns in Portugal

The same penalties as for VAT and Intrastat returns apply. The late submission of ESL returns is punished with a penalty ranging from EUR 150 to EUR 3,750.

The above penalties are regulated in Article 116 RGIT (REGIME GERAL DAS INFRAÇÕES TRIBUTÁRIAS).