EU VAT triangulation simplification

Triangulation allows businesses to reduce VAT registrations in Europe when making international supplies of goods. This is a simplification at the EU level with standard conditions in all EU countries, but some differences apply.

What is triangulation?

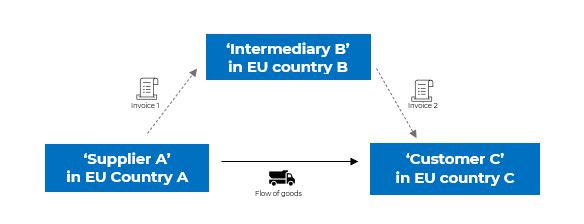

Triangulation is a supply chain transaction where goods are shipped directly by the supplier (party A) to the end client (party C) but invoiced to an intermediary (party B), who then re-invoices this supply to the end customer (party C). In VAT triangulation, there is always one flow of goods and two flows of invoices.

According to the general rules, the scenario above would require a VAT registration of the intermediary in the country of the end client – party B should register in country C -. But triangulation allows party B to avoid such VAT registration. This is to declare an intra-Community acquisition followed by a domestic supply to the Customer in country C. If the customers are in different EU countries because the original supplier ships the goods to multiple customers in different EU countries, the intermediary would need to VAT register in each of these countries.

Check other VAT simplifications implemented in the EU in our dedicated articles for EU call-off stock simplified rules, and OSS VAT returns.

What is VAT triangulation simplification in the EU?

When triangulation simplification applies, the intermediary can avoid a VAT registration in the country of its customer.

From a transaction perspective, these are the conditions to consider a triangular transaction:

- Party A, party B, and party C are all VAT registered in three separate Member states.

- Goods are directly shipped from party A to party C. The transport is arranged by party A or party B.

- An invoice is issued from party A to party B. A second invoice is issued from party B to party C.

- Party B is not VAT registered in country A or country C. There are different interpretations of this requirement, and some countries allow the intermediary to be registered in countries A or B. Contact Marosa to get an overview of this requirement.

If conditions for VAT triangulation simplification are met, the intermediary or party B avoids a VAT registration in country C, where the goods arrive.

If conditions are met, triangulation simplification laid down in Article 141 of the EU VAT Directive applies, and party B does not have to be registered for VAT in country C, where the Customer is located.

VAT Triangulation after Brexit

The UK is no longer part of the European Union after Brexit. Consequently, where a UK business is involved in a triangular supply chain transaction, triangulation simplification on VAT cannot apply because at least one of the conditions is not met.

Party A, party B, and party C involved in the transaction must all be VAT registered in three separate European Union Member states; in consequence, triangulation cannot apply when one of these parties is registered in the UK.

However, UK companies can continue to benefit from the triangulation simplification if they have a VAT number in a Member State country involved in the supply chain transaction. This VAT registration should be in a country different from country A or country C.

UK companies may continue to use the triangulation simplification if they have an EU VAT number in place.

How does VAT triangulation work in practice?

From a VAT perspective, the triangulation from article 141 of the EU VAT Directive works as follows:

Original supply – Company A in EU country A

- VAT treatment: There is a zero-rated intra-Community supply (or ‘ICS’) from company A to company B.

- Invoicing: A zero-rated invoice should be issued indicating the customer’s (party B) VAT number in another EU country and referring to article 138 of the EU VAT directive

- Reporting: Company A reports the supply in the European Sales Listing return as intra-Community supply. It is also reported in the VAT return of company A. The supply is also reported in the Intrastat return when the Intrastat threshold is exceeded.

Purchase and supply by the intermediary – Company B in country B

- VAT treatment: The purchase is an acquisition under triangular simplification from company A to company B. The supply is a zero-rated triangular supply from company B to company C.

- Invoicing: Company B issues a zero-rated invoice indicating the client’s (party C) VAT number in the country of arrival of the goods and referring to article 141 of the EU VAT directive. Following recent ECJ jurisprudence, it is important that the invoice expressely states that "reverse charge" applies, so the customer self-assesses the VAT on the purchase (C-247/21 Luxury Trust Automobil).

- Reporting: The supply is listed in the European Sales Listing return by company B as triangular supply (use code T or equivalent in your country). Some countries (only a few) require this purchase and supply to be reported in the VAT return. This purchase and supply are not reported in the Intrastat return.

Final purchase – Company C in country C

- VAT treatment: Purchase under the reverse charge mechanism. There is no VAT charged on the invoice.

- Invoicing: Not applicable.

- Reporting: The purchase is reported as a reverse charge acquisition. Company C will manually calculate the VAT amount and report it as deductible and payable VAT (both) in the VAT return. The net result will be nil unless Company C does not have full right to deduct.

VAT triangulation examples

For example, party B is a French-established company that receives an order for clothing products from party C, a Spanish company. The products are manufactured in Italy by supplier A. Although B sells the goods to C, the goods are directly dispatched from A – in Italy to C – in Spain.

Usually, according to the general VAT rules, the French company would need to register for VAT purposes in Spain. But if triangulation applies, the French company will avoid a VAT registration in Spain.

In another example, a UK business that is VAT registered in The Netherlands acts as the middleman between a German supplier and a Polish customer. Goods are shipped directly from Germany to Poland. Even if the UK business is based outside the EU, it can use its Dutch VAT number to apply triangulation and avoid a VAT registration in Poland.

We will call you back

Give us your contact details and our team will contact you to organize a demo and evaluate how you can integrate your system with our tool.