E-commerce

European VAT regulations for e-commerce

OSS scheme allows distance sellers to maintain one single VAT registration and only one VAT return is to be submitted quarterly for sales in all countries.

Still, OSS scheme is voluntary. Therefore, distance sellers who do not join OSS must VAT register in all EU countries where they are selling their goods to final customers, charging VAT at the applicable rate in the country of destination, and submit the correspondent VAT returns in each of these countries.

It is important to note that there are some exceptions to OSS scheme, which we will introduce in the next section: i) transactions made before 1 July 2021, and ii) holding stock in several EU countries, are some of them.

Old e-commerce VAT rules

Old e-commerce VAT rules are applicable for those transactions performed before the 1 July 2021. That is, an e-commerce business must register for VAT in the client’s country when sales in that given country exceed 35,000€ per year – former distance sales thresholds. This threshold had been increased to 100,000€ in certain countries like Germany and The Netherlands.

For example, if a company established in Germany sold products from Germany to French consumers for an annual value of 30,000€ between January and the 30th of June 2021, it does not have to register in France, but if the value of those sales was 36,000€ it would need to register for French VAT and regularize those sales. The same would apply to sales in any other EU country.

Also, if you imported your products from a non-EU country so they are sold to European customers, and you acted as the importer of records, you would normally need to register for VAT in each country.

Holding stock in the EU

For certain scenarios, OSS scheme cannot be applied to avoid multiple VAT registrations. This is especially true for members of Amazon’s pan-European program, as holding stock in another country obligates the seller to be VAT registered in that country. This also applies for distance sellers who are not in the pan-European program but store their products in a warehouse in another Member State.

Anyone holding stock in a foreign EU country would need to register for VAT in the country where they hold stock. Some e-commerce sellers move their products closer to their potential clients so they can make a speedy supply. This is the case for Amazon FBA sellers. In these schemes where the goods are stored in a foreign EU country, a VAT number in that country is always required.

In consequence, members of Amazon’s FBA or pan-European program can benefit from OSS scheme for reporting their Intra-Community distance sales, but this will not avoid VAT registrations in the countries where they are holding stock. This also applies for distance sellers who are not in the pan-European program but store their products in a warehouse in another Member State.

For example, a French online seller, who is holding stock in France, Germany and Spain must be VAT registered in those three countries where he holds stock, and also join to OSS scheme to report the Intra-Community distance sales made from the different warehouses – eg., a sale made from the Spanish warehouse to a private customer in Portugal.

Additionally, special rules apply for marketplaces such as Amazon or eBay.

Threshold

There is an annual threshold of 10,000€ that applies for all Intra-Community distance sales and Telecommunications, broadcasting & electronic services (TBE services).

When distance sales do not exceed this threshold, VAT can be charged at your country’s VAT rate, this is, these intra-Community distance sales will have the same VAT treatment as domestic supplies. However, when that threshold is crossed in another Member State, VAT must be charged at the rate of each country of destination.

If you are performing both Intra-Community distance sales and TBE services, you must account all those transactions to calculate the threshold of 10,000€. Also, this is a global threshold in the sense that it does not apply separately per country of destination, but you must account for all EU Intra-Community distance sales and TBE services made.

Finally, the 10,000€ global threshold can only be applied by Suppliers established, with permanent address or usually residing in only one EU country. Also, the goods must be sent from the Member State of establishment. Therefore, the exemption threshold does not apply if the Supplier is established outside the EU, neither by a Supplier that keeps stock in several EU countries.

One-Stop Shop (OSS) and Import One-Stop Shop (IOSS)

OSS schemes allow e-commerce businesses to have one single VAT registration for their sales in all EU countries. In this sense, all sales in Europe can be reported in a single VAT return and the VAT is paid in a single country.

There are three possible schemes for sellers to join depending on the type of supplies and the country of establishment: Union OSS, non-Union OSS, and IOSS.

It is important to note that these are voluntary schemes, therefore, online sellers making intra-Community distance sales or import distance sales may opt to VAT register in each of the countries of destination of the goods.

Which transactions are covered by the OSS schemes?

When you sell products from your home country to customers in your home country, these sales are not covered by the OSS scheme and will be reported in your usual VAT return. If, however, these products come from another EU country, such sales would qualify as intra-Community distance sales and you would report them in the OSS return.

Other types of transactions that are normally covered under the new e-commerce VAT rules include:

- Distance sales of goods and services to non-taxable person in another EU country (OSS).

- Distance sales of goods imported from outside the EU in shipments below 150€ (IOSS).

Which companies can participate at OSS?

Non-EU businesses, EU businesses, and marketplaces (also known as a deemed supplier) are eligible. It is important to note that depending on the activity to be carried out and where the business is established, one of the three OSS schemes mentioned above would apply (Union OSS, non-Union OSS, and Import OSS (IOSS)).

Benefits of OSS schemes

E-commerce VAT rules in Europe and the OSS regime provide many benefits for participants. They may avoid VAT registering in multiple countries for simply carrying out cross-border transactions. Things like having to register in different countries, keeping track of due dates, making sure the payments are sent correctly and litigating in different languages can cause a big headache for sellers. OSS regimes lessen the burden on sellers while also reducing their administration costs.

At Marosa we can help you

We understand that e-commerce VAT rules can be confusing, especially when trying to figure out how to correctly prepare VAT returns. The good news is that Marosa has an automated and cost-efficient software that will help you to submit all VAT returns automatically with an easy-to-use wizard that will guide you in each filing.

Applicable OSS schemes in EU ecommerce sales

There are different schemes in the European VAT regulations according to the activity and place of business of the seller: Non-Union OSS, Union OSS and Import OSS scheme or IOSS. All three schemes are reported in the same OSS return, but they cover different scenarios as explained below.

Which OSS scheme applies to your business?

Different VAT schemes apply for e-commerce businesses depending on the type of activity and country of establishment.

Businesses that are established in the EU can use the Union scheme and the Import scheme, whereas taxable persons who are not established in the EU can possibly use all three schemes, i.e. the non-Union, the Union and the Import scheme.

Non-Union OSS scheme

Union OSS scheme

Import OSS scheme or IOSS

How does each OSS scheme work?

Although all transactions falling into any of the OSS schemes are reported in the same OSS return, each scheme is foreseen as a simplification for different activities:

- Non-Union scheme: Allows non-EU businesses to register in a single country and report all sales of services to private individuals in a single VAT return. This scheme used to apply only to electronic services, but is now available to all services including entrance to events, transport services, etc.

- Union scheme: Allows EU and non-EU businesses to report their sales of goods from an EU country to a final customer in another EU country in a single VAT return.

- Import scheme (IOSS): Allows exempt imports of products that are sold to private individuals in foreign EU countries when the shipment is below 150€. The customs declaration is also simplified. If the value is above 150€, normal rules apply (full customs declaration and import paid at the border, a VAT registration may be required).

OSS registration in the EU

How to request an OSS registration in the EU

You can register for the OSS electronically by submitting an application form to the tax authorities of your country of OSS registration. Each Member State will evaluate the conditions to be met and will approve the OSS registration submitted in his jurisdiction.

If you register for using the Non-Union scheme or the Import scheme, you will receive an individual VAT identification number from the Member State of identification. If you register for the Union scheme, no separate individual VAT identification number will be attributed. Your usual local VAT number should be used.

In which country should you register for OSS?

The country of registration depends on the country of establishment of the business registering for OSS:

- EU businesses should register for OSS in their country of establishment

- Non-EU businesses can choose in which EU country they register for OSS. If a non-EU business uses the Union scheme, it should register in the country from where the goods are dispatched (or one of them if the goods are dispatched from more than one country). Also, if the non-EU business uses the import OSS, an intermediary must be appointed.

Threshold on OSS European regulations for e-commerce

If your distance sales of goods do not exceed 10,000€ in a given year, you do not have to register in the OSS scheme. You will be able to continue charging VAT at your usual country of establishment VAT rate.

This threshold only applies to EU established companies. It is calculated by adding the total amount of intra-Community distance sales of goods and total amount of B2C services. Therefore, you should not consider local sales, exports or other revenue in this threshold.

You will find more information about this threshold on a previous section of this manual.

How does VAT work on sales via online marketplaces in Europe?

When you are selling your goods online via an online marketplace, the rules may deviate from the general VAT regulations for e-commerce in Europe.

Sales of goods made via an online marketplace such as Amazon or eBay will, in some cases, make the marketplace liable for VAT on that supply. This means that it is the marketplace, and not the seller, who will collect VAT from the final client and transfer that VAT amount to the relevant tax authority.

When is the marketplace liable for VAT?

A marketplace is considered to be involved in a supply when it sets the terms of the supply either directly or indirectly, it is involved in authorizing the payment, or it is involved in the delivery of the product. Meeting any of these three conditions would mean the marketplace is considered as involved in the supply.

When the marketplace is involved, there are two scenarios in which the marketplace becomes liable for collecting and paying VAT:

- Sales of goods by a non-EU e-commerce seller made via an online marketplace.

- Goods imported into the EU with a shipment value below 150€ to be sold to an EU customer via an online marketplace.

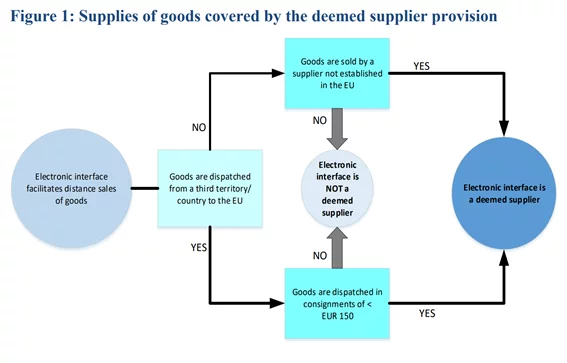

The chart below was published by the European Commission to illustrate the scope of the marketplace liability:

Mechanics of the deemed supply between the ecommerce seller and marketplace

When the marketplace is considered to be liable for the payment of VAT, there is a fiction of purchase from the online seller and supply to the final customer. This is deemed a purchase and a sale considered only for VAT purposes.

The supplier will make an exempt sale to the marketplace. The marketplace will then charge and collect VAT from the final client.

Regarding invoicing requirements, the following scenarios can take place:

Leg 1: Deemed supply to the online marketplace.There two scenarios:

- Distance sales of imported goods: This is an exempt supply. No need to issue an invoice. This supply is outside of the EU VAT rules.

- Supply of goods within the EU by a non-EU supplier: An invoice should be issued by the supplier to the marketplace. The Commission already confirmed that self-billing arrangements can be made according to local invoicing rules in the relevant country.

Leg 2: Deemed supply by the online marketplace to the final customer.There are also two scenarios:

- Distance sales of imported goods: The marketplace should charge and collect VAT at the applicable VAT rate. This is a B2C supply so there is no obligation to issue an invoice, although some Member States may still impose the issuance of an invoice according to Article 221 of the VAT Directive. Contact us to know in which countries an invoice would be required.

- Supply of goods within the EU by non-EU supplier: There are two options applicable in this scenario:

- a) Domestic supply of goods: An invoice does not have to be issued unless the country requires it according to article 221;

- and b) Intra-Community distance sales of goods according to the Union OSS scheme: An invoice does not have to be issued. In the unlikely case that this supply is not treated under the Union scheme, an invoice will be required.

The rules are similar to those already applicable in the UK.

The role of an intermediary for European VAT

In some cases, an intermediary should be appointed by non-European sellers to comply with EU VAT rules.

Suppliers from outside the European Union established in a country with which the EU has not concluded a mutual assistance agreement must appoint an intermediary in order to use the Import OSS scheme.

The intermediary is jointly and severally liable for the payment of VAT to the relevant tax authority. In practice, it is this intermediary who will submit the IOSS returns. It is not required that the intermediary takes care of the customs declarations of the supplier.

Marosa has an intermediary tax identification number and we will link it to your IOSS VAT number in order to represent your business in the IOSS scheme.

European VAT rules for Amazon sellers

If you are an Amazon seller, your VAT obligations in Europe are driven by the following rules:

- Ecommerce VAT rules and OSS schemes for ecommerce sales in the EU

- Role of marketplaces on ecommerce supplies in the EU

- Obligations arisen from the stock held in other EU countries when using the Amazon FBA program.

The first two regulations are explained in the articles linked above. We are providing explanations below of the FBA impact on VAT rules for Amazon sellers.

Marosa automates your VAT obligations and identifies the VAT treatment of each of your transactions in Europe. Contact us to know more about how we can help you staying on top of your VAT compliance obligations in Europe.

Marosa automates your VAT obligations and identifies the VAT treatment of each of your transactions in Europe. Contact us to know more about how we can help you staying on top of your VAT compliance obligations in Europe.

What is Amazon FBA?

FBA stands for Fulfilment By Amazon. The Amazon FBA program offers sellers the possibility of a quick and hassle free delivery to all customers around the world. To make this happen, an Amazon seller will place his or her products in the nearest Amazon warehouse. Amazon will then distribute the goods across warehouses in other countries so that they are closer to the final customer and can fall in the category of "Amazon prime" (shorter delivery times).

There are clear opportunities and economic benefits of this scheme, but you should also be aware of additional obligations in the field of VAT.

VAT rules for Amazon sellers who are not in the pan-European FBA program

If you do not outsource the logistics of your sales to Amazon and you only use this platform to advertise your products, you will fall in the general rules of VAT under the OSS regime in 2021.

You can read this manual considering the general rules and you do not have to worry about the exceptions explained immediately below. That is, you can still submit a single OSS return where all sales across Europe are reported and you will not require additional VAT registrations, unless you keep stock in several EU countries.

VAT rules for Amazon sellers who are part of the pan-European FBA program

If you benefit from the Amazon FBA program and your products are stored in Amazon warehouses abroad, you will need to register for VAT purposes in each of the countries where your products are stored.

In practice, this means that you cannot benefit from the full simplification of OSS for online sale of goods, but the good news is that part of your sales would still fall within this simplified regime.

Here are some rules that you should consider:

- You will need to submit two types of VAT returns: 1) A single OSS return for all intra-Community distance sales of goods; and 2) regular VAT returns in each country of registration for “movements of stock” and “local sales in that country”. You will also submit a regular VAT return in your home country.

- Intra-Community distance sales from any Amazon warehouse to a customer abroad (outside the country where the warehouse is located). Those sales will be included in your OSS return as explained above.

- Your movements of stock (FC_Transfers) need to be reported in each country where the movement takes place. So, for example, if Amazon moves stock from a German Amazon warehouse to a French Amazon warehouse, such movement must be reported as an intra-Community dispatch in your German VAT return and as intra-Community arrival in your French VAT return.

- Your local sales are those sales made from an Amazon warehouse to a customer located in the same country where the warehouse is located. For example, a sale from your French Amazon warehouse to a French customer would fall in this category.

- You should also consider any supply where Amazon is considered the deemed supplier, as this will deviate the VAT treatment of your sales.

You can find all the information about the type of sale you are making in the Amazon VAT transactions report. More information about this report is available on Amazon's website.

The good news is that Marosa has an automated and cost efficient software that will help you submitting all VAT returns automatically with an easy-to-use wizard that will guide you in each filing.

Contact our Amazon team to know how we can help you.

Example of VAT obligations for Amazon sellers in the FBA pan-European program

Company C is an Italian business that ships its products to Amazon Italian warehouses so that they are distributed across the EU as part of the FBA program.

Company C holds stock in all Amazon marketplaces in Europe, so it must be registered for VAT in all these 7 countries (UK, Spain, France, Germany, Poland, Czech Republic and The Netherlands).

In April 2021, Company C downloaded the Amazon VAT transactions report for March and took note of the following activity carried out during March (to keep it simple, we included 0 sales in most countries, but we are sure your business does better than that!):

*We only included two sample columns (Spain and Belgium) but you will get multiple columns, one of each country.

If we only take into account the above sales, the following returns will be submitted by company C:

Individual country by country returns:

In this example, Company C will make three separate payments. The OSS payment to the Italian tax authorities for an amount of € 16,800, the German VAT return payment for € 380 and French VAT return payment for € 1,800.

Company C will also file nil VAT returns in Spain, UK, Poland, Czech Republic and The Netherlands. Also, a regular VAT return will be submitted in Italy in addition to the OSS Italian return. And if that was not enough, an ECSL return must be submitted in Germany and DEB return in France (if thresholds are exceeded).

In all these scenarios we took the standard VAT rate as an example, but remember that different VAT rates apply depending on the product sold in each country.

Remark on VAT rules on B2B sales by Amazon sellers

Amazon is expanding sales to business customers. This is an opportunity to increase sales and profits, but also VAT rules should be regarded as the VAT treatment on these sales and will deviate from the standard rules on OSS regime and distance sellers.

When you sell your products to business customers using your Amazon seller account, the VAT treatment will depend on whether you use Amazon FBA or not. None of the sales described below would be reported in the OSS return.

If you do not use Amazon FBA on your B2B sales:

- Sales to customers abroad: You will treat them as intra-Community supplies from your home country. VAT will not be charged if the exemption conditions are met.

- Sales to local customers: You will treat as domestic sales. VAT will normally be charged at your home country's VAT rate.

If you use Amazon FBA on your B2B sales:

- Sales to customers abroad (includes any sale from an Amazon warehouse to a business customer located in a country different from the country of the warehouse of dispatch): You will treat them as intra-Community supplies from your home country. VAT will not be charged if the exemption conditions are met. These sales go in your standard VAT return of the country of dispatch (not your OSS return).

- Sales to local customers (includes sales from an Amazon warehouse to a business customer located in the same country of the warehouse of dispatch). There are two options: a) You charge VAT at the local rate of the domestic country; or b) You do not charge VAT because domestic reverse charge applies.

All the above is complex, but Marosa's tool will automate the reporting of all your sales in Europe with a hassle-free solution. We also will integrate with your Amazon seller account so you do not have to worry about providing the information.

Get help from Marosa

Amazon provides a great infrastructure to grow your business and to put you in contact with an unlimited number of sales opportunities. However, VAT rules get complex among all possible scenarios and administrative rules. Multiple VAT returns and registrations make it difficult to focus on your strategy and business growth.

Thankfully, Marosa has a dedicated team and fully automated tax technology solution that will take care of all your VAT obligations. You will simply receive a notification with the amount to be paid each period to the relevant tax authority. Everything else, including VAT registrations, data collection, VAT returns, ECSL returns, Intrastat, and archiving of all your documents will be handled by your dedicated Marosa manager.

We rely on technology, but we are not technology. We are VAT experts who analyze your transactions carefully and provide an individual service to you personally.

Contact us to know more about how we can help you and request a free demo of our tools and processes.

VAT rates in ecommerce when using the OSS schemes

Once you are registered in the OSS regime for online sales of goods, you must charge VAT using the applicable rate in each country of consumption. For example, if you sell photobooks in France and Germany, you should ensure that the correct rate is charged on each sale according to the local rules in Germany and local rules in France.

The scope of reduced VAT rates is different from one country to another in the EU. There is an increased complexity where a product has a miscellaneous nature. For example, in our example above on Photobooks, it is possible that these books have a combination of text and photos. In these cases, you should evaluate carefully if you should consider them a book (often super-reduced rates) or photobook (reduced or standard rates).

It is important that you carry out a study of the applicable VAT rates on your products across the EU. Using the wrong rate can give raise to penalties or long disputes with the tax authorities to reclaim VAT that has been overcharged by mistake.

Marosa has extensive experience on the scope of reduced rates in each European country. We will create an overview with the applicable VAT rates according to existing legislation with a pan-European approach that is consistent for all Europe. Contact us to get help with your study of VAT rates.

All you need to know about OSS VAT returns

An e-commerce seller using one of the OSS schemes needs to submit an OSS return declaring all sales falling under the scope of the OSS rules. These OSS return includes VAT charged under the VAT rates in each country of consumption.

In practice, the e-commerce seller will report to the tax authorities in his or her home country (or country of registration if he or she is a non-EU seller) how much VAT he or she owes to each tax authority of the country of consumption. A single payment will be made for the total sum of VAT due across Europe. The tax authority of the country where the OSS return is submitted will then transfer the amount to the country of consumption according to the information reported in the OSS return.

Content and currency of OSS returns

The OSS return has a standard content and structure in all EU member States.

OSS returns are completed using one currency only. This will often be EURO, but some Member States may require OSS returns to be completed in their local currency. In those countries, the exchange rate published by the European Central Bank should be used.

The content of the OSS return is split in sections according to the sales made under each scheme.

- The Non-Union scheme will include supplies of B2C services by non-EU companies to customers in another EU country.

- The Union scheme will include a) supplies of B2C services by EU established companies to customers in another EU country; b) intra-Community distance sales of goods; and c) deemed supplies made by marketplaces.

- The Import OSS scheme will include distance sales of goods imported into the EU where the shipment value is below 150€.

It is not possible to deduct VAT in the OSS return. VAT incurred on purchases must be deducted via the domestic VAT return or via the EU mechanism to recover VAT incurred abroad.

Frequency of OSS returns

As a general rule, OSS returns are submitted quarterly according to calendar quarters. Calendar quarters are January to March, April to June, July to September, and October to December.

OSS returns when using the Import OSS scheme are submitted on a monthly basis.

Deadline of OSS returns

OSS returns are due by the last day of the month following the reporting period. For example, the Q1 OSS return is due by 30 April, and the Q3 OSS return is due by 31 October. Likewise, monthly OSS returns are also due by the last day of the month following the reporting period.

If the due date falls on a bank holiday or weekend, this deadline is not shifted to the next working day.

Payments of VAT in OSS returns

The payment of all VAT due reported in the OSS return is made to the tax authorities of the EU country of OSS registration.

In practice, a unique reference is provided by the tax authorities once the OSS return is submitted. This reference must be used in the payment of the VAT due resulting from this OSS return.

The payment must be made and reach the tax authorities bank account before the due date to submit the relevant OSS return.

Penalties for late payments and late filing of OSS returns

If an OSS return is submitted late, the tax authorities in the country of identification will send a reminder electronically on the 10th day following the date on which the OSS return should have been submitted. Any further reminders will be issued by the Member State of consumption. Also, penalties will be assessed and imposed by the Member State of consumption.

In case of late payments of OSS returns, the seller will also receive a reminder on the 10th day following the due date to make the payment. Further penalties for late penalties will be assessed by the tax authorities in the country of consumption. If the EU country of consumption sends a reminder, the VAT due must be paid directly to the tax authorities of that specific Member State.

You should also take into account that the OSS registration can be cancelled in case of persistent omissions in your OSS returns.

We will call you back

Give us your contact details and our team will contact you to organize a demo and evaluate how you can integrate your system with our tool.